How to Form an Investment Bank in Ethiopia: Capital, Licensing and Talent Requirements

Ethiopia’s capital market now has a defined rulebook for launching an investment bank. Here is what founders need on paper, in the bank account, and on staff, set against the standards used in mature markets.

Why This Question Is New for Ethiopia

Until recently, “investment bank” had no formal meaning in Ethiopian law. That changed with the Capital Market Proclamation No. 1248/2021, which created the Ethiopian Capital Market Authority (ECMA), and with the launch of trading on the Ethiopian Securities Exchange (ESX) in January 2025. Investment banking is now a licensed activity under ECMA’s Capital Market Service Providers Licensing and Supervision Directive No. 980/2024, alongside brokers, dealers, custodians, portfolio managers and fund operators. By early 2026, ECMA had licensed 16 institutions across investment banking, advisory and brokerage, including bank-owned entities such as CBE Capital and Wegagen Capital Investment Bank, with the first international applicant’s paperwork already lodged.

Legal Form and Registration

An applicant must be a share company or a private limited company holding a valid commercial registration certificate, or an investment permit where relevant. Before any license is granted, ECMA conducts a pre-certification inspection to confirm the applicant’s governance, systems, and paperwork meet the standard. Firms intending to broker must also show an Approval-in-Principle for trading membership from the ESX or another recognized trading facility.

Core documentation includes a business plan, audited or projected financial statements, identification and beneficial-ownership records, internal manuals covering operations, trading, ethics and anti-money-laundering controls, and record-keeping systems. Industry guidance puts the paperwork at more than 16 supporting documents for a complete application, and ECMA reviews foreign and domestic applicants on the same non-discriminatory criteria.

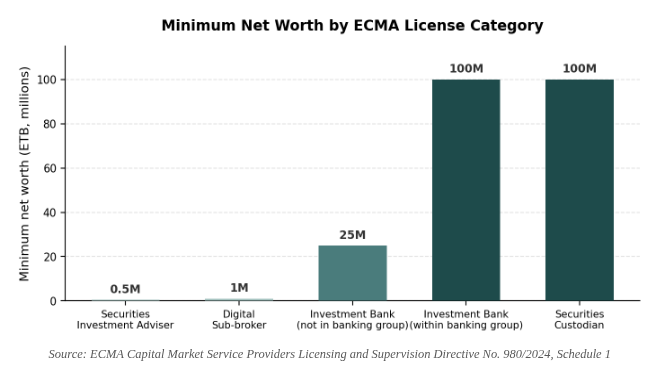

The Capital Question

ECMA sets minimum net worth by license category under Schedule 1 of Directive 980/2024, and the required cash must sit on deposit in a licensed Ethiopian commercial bank before licensing. Investment banking sits at the upper end of the scale, on par with custody, because both functions carry systemic and client-asset risk.

Source: ECMA Capital Market Service Providers Licensing and Supervision Directive No. 980/2024, Schedule 1

| License category | Min. net worth (ETB) | Notes |

|---|---|---|

| Investment bank (within a banking group) | 100,000,000 | Applies where the parent or an affiliate is a licensed bank |

| Investment bank (standalone) | 25,000,000 | Applies to firms with no banking group affiliation |

| Securities custodian | 100,000,000 | Highest tier, reflecting asset safekeeping risk |

| Collective investment scheme operator | 25,000,000 | Fund and asset managers |

| Portfolio manager/appraisal firm/credit rating agency | 15,000,000 | Mid-tier advisory and valuation functions |

| Crowdfunding intermediary | 6,000,000 | Reflects smaller transaction sizes |

| Securities digital sub-broker | 1,000,000 | Entry-level brokerage tier |

| Securities investment adviser (corporate) | 500,000 | Lowest capital bar in the framework |

The Human Capital Requirement

Capital buys the license; people keep it. Directive 980/2024 sets out a Competency Framework for Capital Market Service Providers, under which every functional role, from research to compliance to trading, must meet defined qualification standards, and firms must maintain continuing professional education for licensed staff.

- A qualified board of directors must meet the competency standards ECMA sets for governance oversight, not just company law minimums.

- A licensed Trader: any investment bank acting as a broker must have at least one licensed Trader serving as Appointed Representative, skilled in corporate finance activity.

- A separate Chief Compliance Officer: this role is excluded from the Trader function, so one person cannot hold both.

- Written manuals: operations, trading, ethics, anti-money-laundering, and record-retention policies must exist before licensing, not be drafted afterward.

- Client-protection controls: firms cannot exercise discretion over client accounts or accept instructions from anyone but the client without written authorization.

Measured Against the Global Standard

Ethiopia’s framework is new, but it draws on international practice. In the United States, a comparable firm registers as a broker-dealer with the SEC and joins FINRA, which enforces its own net capital, staffing, and supervisory rules on top of the federal floor.

| Requirement | Ethiopia (ECMA) | Global standard (US model) |

|---|---|---|

| Regulator | Ethiopian Capital Market Authority (ECMA) | SEC, with FINRA as a self-regulatory organization |

| Core rulebook | Directive No. 980/2024 | Securities Exchange Act, SEA Rule 15c3-1, FINRA Rules 1210/1220 |

| Minimum capital, standalone firm | ETB 25,000,000 (roughly USD 170,000 to 190,000) | USD 5,000 to 250,000+, higher for underwriters and carrying firms |

| Legal form | Share company or private limited company with commercial registration | Broker-dealer entity registered via Form BD |

| Individual licensing | Trader as Appointed Representative: Role-Based Competency Framework | Series 79 investment banking exam, plus SIE and principal exams |

| Compliance officer | Chief Compliance Officer required, cannot double as Trader | Chief Compliance Officer registration is mandatory on Form BD |

| Minimum principals | Competent board under ECMA’s competency framework | At least two officers registered as General Securities Principals |

| Pre-licensing check | ECMA pre-certification inspection | FINRA new-member application review |

The comparison shows convergence on principle, tiered capital by risk, named compliance accountability, licensed individuals and not just licensed firms, even where the absolute figures and exam regimes differ. Ethiopia’s ETB 25 million standalone threshold (roughly USD 170,000 to 190,000 at mid-2026 exchange rates) sits above the US entry-level minimum, but well below the capital a firm running underwriting or proprietary trading would need in either market.

The Formation Path, Step by Step

- Incorporate as a share company or private limited company and secure commercial registration.

- Complete ECMA’s self-evaluation questionnaire to test readiness against governance, financial, and operational standards.

- Deposit the required minimum net worth in a licensed Ethiopian commercial bank.

- Recruit and document a competent board, a licensed Trader if brokerage is intended, and a dedicated Chief Compliance Officer.

- Draft internal manuals: operations, trading, ethics, anti-money-laundering, and record-keeping.

- Submit the full application, business plan, and supporting documentation to ECMA for review and pre-certification inspection.

- If brokerage is intended, obtain Approval-in-Principle for trading membership from the ESX.

- Receive the license, then maintain continuing professional education and capital adequacy on an ongoing basis.

The Bottom Line

Forming an investment bank in Ethiopia is no longer a theoretical exercise. It is a defined, document-heavy process built around three pillars: legal registration, risk-tiered capital, and named, qualified individuals, that mirrors the logic used in established markets even as the specific numbers and exams differ. With 16 institutions already licensed and the first international applicant in process, the practical constraint for new entrants is shifting from whether this market exists to whether they can meet the paperwork, capital, and staffing bar ECMA has set.

“This article is for informational purposes only and does not constitute legal or regulatory advice. Applicants should refer to ECMA directives and seek professional advice where appropriate.”